Posted By: AndrewAMD

Broker API - Options Questions - 07/11/17 02:11

Hello,

I'm writing options features into the Ally Invest plugin, and I have three questions:

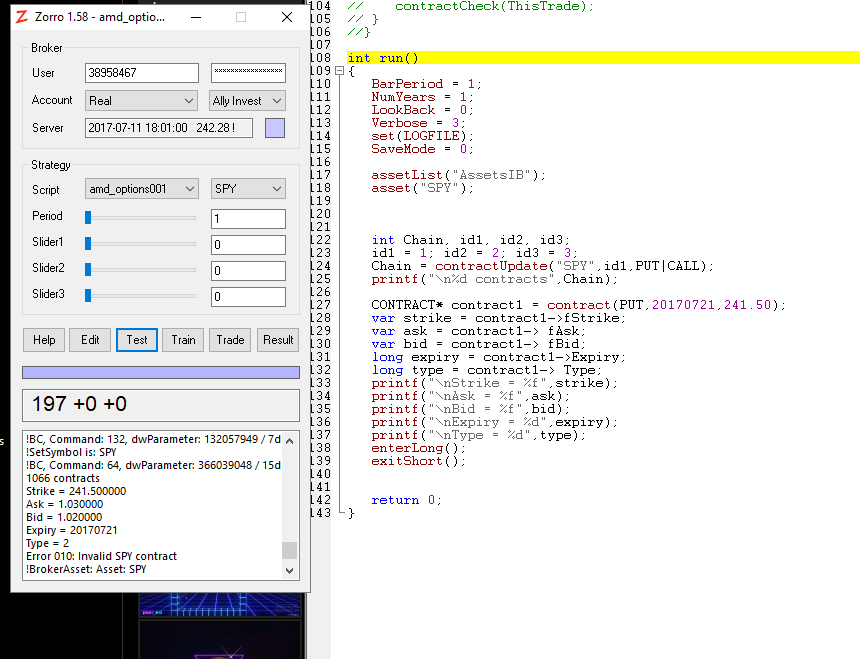

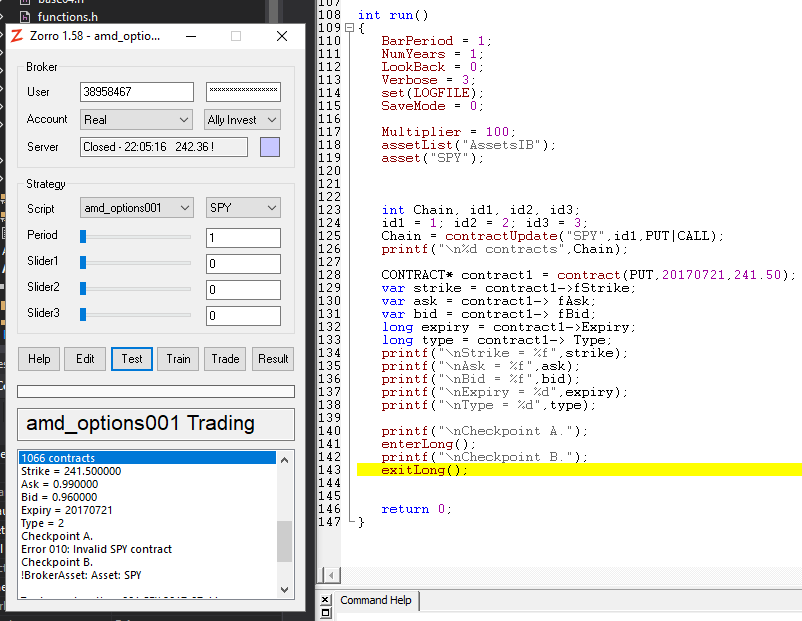

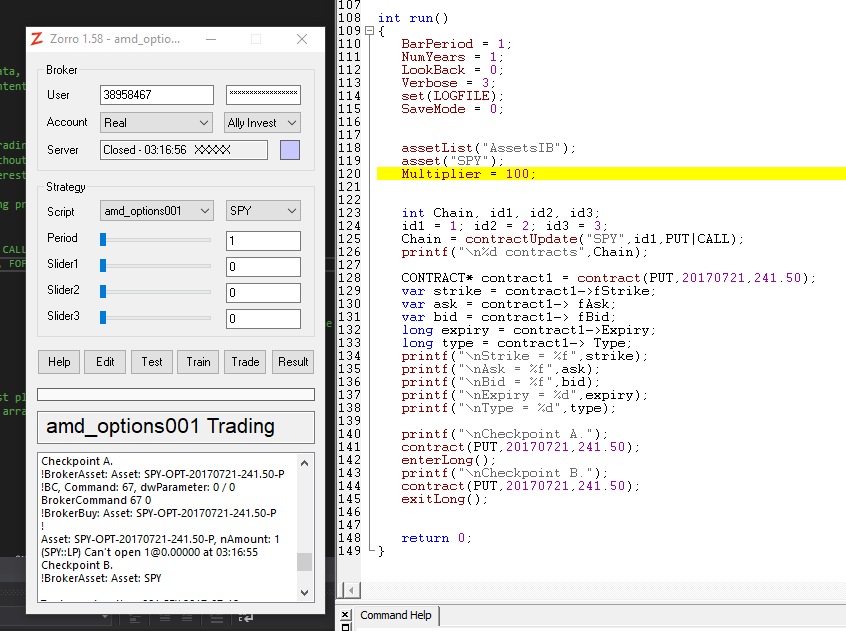

#1 - What is the correct procedure for writing the BrokerCommand GET_OPTIONS function? Am I supposed to build up an array of CONTRACT's and then copy it to the DWORD like so...

If not, please point me in the right direction.

#2 - I see that I have two symbol definitions... One is in SET_SYMBOL, and one is char* Asset. If a user wants to buy/sell an option, would the option symbol be defined in SET_SYMBOL or in char* Asset? Will there be cases where I would have to use one and override the other? Is SET_SYMBOL strictly for usage with BrokerCommand?

#3 - Will a user need the options symbols all individually in the AssetFix.csv file?

I appreciate any clarifications. Thanks.

Andrew

EDIT - I did eventually fix the above snippet. I'll document it here.

I'm writing options features into the Ally Invest plugin, and I have three questions:

#1 - What is the correct procedure for writing the BrokerCommand GET_OPTIONS function? Am I supposed to build up an array of CONTRACT's and then copy it to the DWORD like so...

Code:

BrokerCommand (int nCommand, DWORD dwParameter)

{

// the below code is for nCommand=="GET_OPTIONS"

std::vector <CONTRACT> contracts;

// send request to server,

// get response from server

// parse data into contracts vector

// here's the part I'm not sure about:

dwParameter = (DWORD)contracts.data();

return contracts.size();

}

#2 - I see that I have two symbol definitions... One is in SET_SYMBOL, and one is char* Asset. If a user wants to buy/sell an option, would the option symbol be defined in SET_SYMBOL or in char* Asset? Will there be cases where I would have to use one and override the other? Is SET_SYMBOL strictly for usage with BrokerCommand?

#3 - Will a user need the options symbols all individually in the AssetFix.csv file?

I appreciate any clarifications. Thanks.

Andrew

EDIT - I did eventually fix the above snippet. I'll document it here.

Code:

BrokerCommand (int nCommand, DWORD dwParameter)

{

// the below code is for nCommand=="GET_OPTIONS"

//this next line is a pointer to an array of 10,000 elements.

CONTRACT* contracts_ptr = (CONTRACT*)dwParameter;

std::vector <CONTRACT> contracts;

// send request to server,

// get response from server

// parse data into contracts vector

// I copied vector elements to the pointer, not to exceed 10,000 elements.

int i;

for (i = 0; i < Contracts.size() && i < 10000; i++)

{

contracts_ptr[i] = Contracts[i];

}

return i;

}